Someone pinned this picture on Pinterest of them dividing their money into different envelops as suggested by financial expert, Dave Ramsey. His explanation of the envelope system was simple and made cents/sense, so I thought I’d share it. My thoughts are in PINK, of course. I hope you enjoy!

~Danielle

Get on a Simple System

The key component to Dave Ramsey’s, “Total Money Makeover” is the envelope system. What is the envelope system, you ask? Well, according to Ramsey, its “way to handle money still works. People used to always use cash envelopes to control their monthly spending, but very few do in today’s card swiping culture”. I will say that it works and the comments to post prove it. Check out Ramsey’s simple basics for starting a cash envelope system.

- Budget each paycheck. Budget is a dirty word to most people, but you must budget down to the last dime if you’re going to successfully implement the envelope system. While I know plenty of people who budget a certain percentage of each check, I budget specific figures.

- Divide and conquer. Of course, there will be budget items that you cannot include in your envelope system, like bills paid by check or automatic withdraw. However, you can create categories like food, gas, clothing, and entertainment. I usually work off three main categories: groceries, restaurants/entertainment, personal maintenance (hair, nails, or anything that will help me feel “pretty”). I chose these categories for myself because these are the areas I could be tempted to overspend. I pay my bills off the top and then I budget each paycheck into these categories, which were listed in order of importance.

-

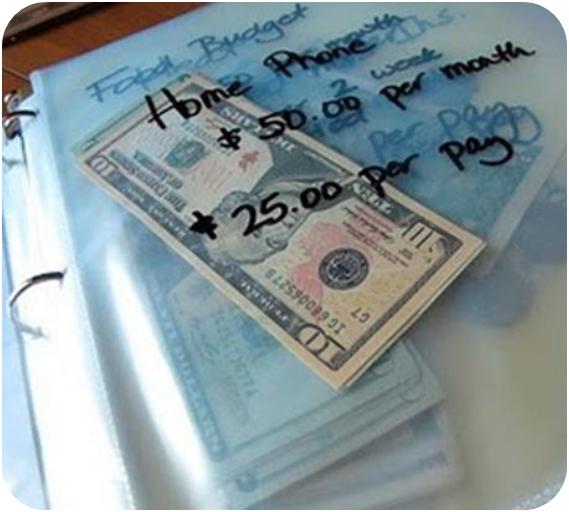

Fill ‘er Up. After you’ve categorized your cash expenses, fill each envelope with the money allotted for it in your budget. For example, if you allow $100 for clothing, put $100 in cash in your clothing envelope for the month.

From Ramsey

When it’s gone, it’s gone. Once you’ve spent all the money in a given envelope, you’re done spending for that category. If you go on a shopping spree and spend the $100 in your clothing envelope, you can’t spend any more on clothes until you budget for that category again. That means no visits to the ATM to withdraw more money!

Don’t be tempted. While debit cards can’t get you directly into debt, if used carelessly, they can cause you to over-spend. There’s something psychological about spending cash that hurts more than swiping a piece of plastic. If spending cash whenever possible can become a habit, you’ll be less likely to over-spend or buy on impulse.

Give it time. It will take a few months to perfect your envelope system. Don’t give up after a month or two if it’s not clicking. You’ll get the hang of it and see how beneficial the envelope system is as you dump debt, build wealth, and achieve financial peace! See … simple! Truth… I sort of fell of the wagon for a while. I actually, couldn’t remember what purse I put the envelopes in until today, when I found them, and I had $20 in my restaurant fund. I started back on the system TODAY!!! It takes work but most great things do….

photo credit: Tales From the Coop Keeper | content: David Ramsey

What are your categories for your envelopes?

FACEBOOK, TWITTER, PINTEREST, RSS Feed,

Email SMC: shemakescents@gmail.com

I switched to the cash system only 2 months ago. I already noticed some difference. I have some extra cash for just in case, and I never had before that. Now, when my “shopping” money is gone, it really is ! One thing only that will bother me is that in my country (Greece) to avoid paying a lot of taxes since most places don’t give a receipt here, the government ask us to pay with debit or credit card. This will cause a huge problem to my system!

Wow!! That’s so interesting that your government encourages you all to pay with a card. I never knew that. By the way, Greece is on my bucket list to visit. I will be starting an envelope for that trip once I’m done paying off my student loans. Nefeli, thank you so much for your comment.

We too use the cash system. Our envelopes are: groceries, booze, blow money his/hers, kids, baby, home/car maintenance and restaurants. Switching to cash has made a huge difference for us. We are on track to pay off our house this month after two years of doing cash. I can’t recommend it enough and even started making and selling my own envelope sets on Etsy. https://www.etsy.com/shop/CraftySundays

That is so inspiring. Image how freeing it will be once you have eliminated your mortgage payment. Thanks for your comment.

I am really fortunate that my bank allows countless “e” accounts. So I do my “envelopes”through my online banking. I have an account for direct deits and then my everyday that my pay goes into and then I have10 or so e accounts which I transfer in and out of!

I rarely deal with cash anymore so this insures I am not tempted to withdraw that $10 extra.

That’s awesome. What bank do you use?

Hi I have a question if you only have minimum wage paying job. I have it to where I pay all my bills on one paycheck and splurge the other. I’ve noticed with this technique that I end up with nothing and I end up being broke! And as bills go i pay Iinsurance on my car and my phobe bill. My bf pays the house bills. What do I do? Have no idea where to start.

Instead of spending all your second check, save half. Save until you have enough to stuff all your envelopes then start

I used to do the same. Then I started splitting my rent (my largest sum) between the two (or if I’m lucky 3) paychecks. I pay it in cash anyway so I would take half out each time.

Now that I have a car payment on top of it I had to rework that a tad. Luckily I now have a job where I make a little more than minimum wage…but not much. I just have to watch my spending a little closer. Its why I’m looking into this system. Lol

Ok, so I am just new to this envelope idea. In fact, today is the first day. Been doing a lot of reading. By biggest concern is how to get started. Right now I have enough in my bank account to cover a car loan, and have a wee bit extra left. I have $60.00 in my wallet. I just paid my cell phone bill and put some money on my credit card. I don’t have a lot of expenses because I live with my boyfriend and he pays the house bills, however, I don’t make a lot of money. I don’t rely on my boyfriends money besides the house bills. I have to pay some school fees for my son’s out of school care at the end of the month. I think I just need to hear someone else say it. Its not just a matter of getting started and organizing, but also of having will power and commitment. Was it hard for you when you first started the envelope system? I feel like I am going to be completely broke for a while and that terrifies me. I mean, my bills will be paid, but I’ll have nothing left. Does the envelope system really work?

Yes it does. My hubby and I have been on the Dave Ramsey program for over 2 yrs. I took on a second job and we were able to pay off $45,000 of debt in 2 yrs. After our debt was paid we started to save for our adoption, in less than 7 months we have half the expenses paid for. I have since quit my second job, so we don’t have the extra income, but we still have money to pay all our bills and still put money away. We both work on commission, so our income is never the same. Using the envelopes helps us stay on track. I have them for groceries, eating out, gas, clothing, dog supplies, beauty products, household/cleaning supplies. I don’t even carry my debit card anymore…takes away the temptation to use it.

Good luck to you!!!

Yes I saved until I had a month worth of envelopes at once.

I have been using this method for years and I am disabled so get my money once a month and it has to last the entire month. The first month I didn’t allocate enough for my food because I just guessed on the amount I had been spending. Thank goodness we have a food pantry in our town. Lol!! I learned from my mistakes as I went along. I was self-employed for years and was used to getting paid weekly. Now if it’s not in my budget it’s just not there, period. I have found ways around and through. Instead of eating out every month, I put $5 each month into that category until I have $15-20 and then I go out. I have learned not to buy a lot of things I don’t really need. It helped to make a list of needs and wants. That way, I will ask myself if I really need it, and I rarely do. Once I leave the store I never think about what I didn’t get, but I focus on being grateful and content. I know where all the best Thrift shops are and in summer I love going to yard sales where I often find great books, craft materials, etc!! I borrow movies from my library in addition to books, music c.d.s., etc. Life is so much simpler now! I find I enjoy the things I get more than I did when I had money to buy things I wanted. It’s fun to look for free or practically free things to do too!! Enjoy the process:-)

Got this article as a pin in my feed this morning, read it and ALL the comments, stopped at Barnes and Noble, picked up the “TMM” audiobook and already listened to the entire book. So many great tips, realities, scenarios etc. Used to discipline myself on a very similar cash system, but ‘failed’ when income became sporadic. Fortunately in a better situation now (knock on wood). However, now staring down the barrel of a “college gun” next year for my senior, it’s time to get on a system again, get hubby involved and stick with it. Hubby has agreed to listen to book too, that is a huge step! Heading back this week to pick up the workbook & get started. Thank you for the article and everyone’s tips in comments! Very inspiring!

Good for you! TMM has help me shape my own views of money and how I handle it. Good luck on your journey to financial freedom.

I stumbled on this process on my own (didn’t know about Dave Ramsay or anything), and I love it! My favorite part is that if I don’t use all the money in one of the envelopes (for example, I budget $15 a day for “weekend food,” but I only use $10 of it), the other five can go in my “savings” envelope. It encourages me to use less money if I can, and I can save even more!

I use envelopes (cash) for groceries, eating out, fun $, and chore $ for the kids…. I realized that I mess up when I don’t put enough cash in there… I try to make our budget too tight thinking we should save a ton!!! but… not being realistic… then I get super frustrated. So… for me it helped me to be realistic!! And leave debit card at home… And leave half of grocery money at home… because I don’t buy enough for the whole 2 weeks… I like to shop each week.

I use this method but not in cash- i use it in Quicken by adding “phantom accounts” for all my budgeted items. I set aside money each paycheck for the “must” bills, then I can use only what is left for other things. One of the “musts” is savings. When it is time to pay the bill, (ie mortgage) I release the funds I have set aside in the phantom account – and pay the bill. It works great and has allowed me to always be able to pay my bills on time and in full. It does mean my “fun” money is very limited but it is worth it to be able to keep a roof over my head, food on the table and no bill collectors at my door. Great system.

You might try using classes in Quicken. I create a class for each virtual envelope and divide my income into them and then add the class to each expenditure. Then I create a class report that tells me how much is in each envelope at any given time–I just have to change the current date to get it up to date if I keep the report saved.

Am I able to get the spreadsheet too? pamela-leitch@hotmail.com

Question…how do you budget make alotments when your paycheck is never the same? My husband works in the contracting world…paid weekly…however, there are rain days, safety stand down days, sickness…in which he receives no pay for the day….how do you do this when there is no base amount to work from?

1) Create budget using a low monthly amount – what he might get in a slow month. When you have extra – you can put that toward a nonessential category or use it as emergency fund to save for a rainy day.

OR —

2) Budget last month’s income. For example, save the income from September in one envelope until the 1st of October, then distribute to the appropriate envelopes for spending.

I would probably use percentages then. I used to do all contract work and that seemed to work well for me, I knew I would make at least $250 per paycheck but $50 had to go towards my phone bill. The rest was 25% for this, 15% for that… hope this helps.

That’s my problem! My husband drives a truck over the road and his check is never the same! It just depends on what his DM can find hi to run and if all goes well. He runs into traffic, maintenance problems, and problems at shippers. ‘

You can still budget on a inconstant income. My wife and I are both servers and we have been using the Dave Ramsey budgeting system for 3 years. Its amazing at how much better quality of life is when you have a system in place that helps you get ahead. Its no longer a balancing act.

Here’s the form from Dave Ramsey for budgeting with irregular income. It works. http://www.daveramsey.com/media/pdf/irregular_income_planning.pdf

We don’t actually do this, but we do something equivalent. We have a few different accounts where our money is direct deposited. We have a ‘bill account’ where half the money for bills is deposited every two weeks. (That means twice a year we have an extra check to do whatever with.) We estimate high so that even the highest electric bill can be paid at any given time of the year. The rest of the months will have extra money in that account but the extra helps with odds and ends of bills like pharmacy, dog grooming, medical bills, etc. Then we have an ‘extras account’ where we build up money to go toward extras–be it trips, household purchases, etc. We also have a ‘savings account’ for our son and a ‘main account’ where the money in the main account goes for groceries, gas, etc…those bills that do not have a set amount each month. If we want to save more at any given time, we just adjust the allotments with my husband’s pay. If more money is needed in any one account, we either transfer it or adjust the allotment for that account. This helps with those using the envelope method who have had people take their money. We don’t have the money laying around the house so it’s not a problem. Also, we use the bank accounts that are completely free…no fees associated with the accounts. Having access to balance them online makes keeping track of our money that much easier, too. Just food for thought…

Hey, I just saw your post on your blog and I am putting it to good use for my own household and blog.

When do you refill the envelopes?

You decide based on what works for you and your family. My husband and I follow this system, and since we are paid every two weeks we budget and fill envelopes for a two week period. We refill them on our next paycheck and make it work for two weeks time till the next check. You could separate it by week or month. We also have other envelopes for things to save for like car taxes that we know will be due. We just add the budgeted $ amount for the month to those envelopes. Money for car taxes ends up not getting spent that way!

I refill EVERY pay day or that Saturday morning after it. When I wait, i get off track because I start swiping my debit care, which is a no-no.

My Parents started doing this 65 years ago and worked well for them. I learned early on to do this and it works. When the $$ is gone, It’s gone! My parents lived frugally but well. They were millionares when they passed away. Hope I can do the same…On our way!

Why would anyone down vote your comment? Jealous that your parents became millionaires because of their frugal lifestyle? Good for them!

I started this two months ago and it’s amazing! I’m a college student who goes to school full time and gets paid minimum wage and I decided I wanted to save up for a mission trip and a new digital camera. Seemed a little impossible at first but I decided to split up my paycheck, but enough in the bank for gas(that’s the only thing I use my debit card for now) and I percentage ill take out and put in my savings account. Then everything else I split up into envelopes by percentages of my paycheck. I have a beauty(everything from clothes to make up to spa days), food, entertainment, gifts, tithe, missions, camera. I think that’s all but I’m already half way toward getting a camera! AND I just feel so much more at peace knowing I’m only spending whatbibhave and saving up.

It does take some adjusting too though and is a bit of a wake up call! Ya night think twice you go to get a $5 dlar Starbucks! Haha

Finally another college student! It’s hard because so many budgets are made for people who make real money and not 6-10k in a full year!

I do a mixture of both. I pay all my bills online, but every paycheck I go to the bank and take out the “extra” money. When I get home the extra goes into envelopes. (Date night, dog grooming, travel, kids) My boyfriend gives me a set amount each of his paychecks to cover all the birthday and xmas gifts for our kids (we have six between us and one grandchild). That way when a birthday pops up, we already have the cash to go buy a giftcard or whatever. As far as bill paying goes, we each have our own checking account where our paychecks are direct deposited and then we have a joint account where we transfer our share of the household money. So rent, groceries, utilities all get subtracted from that account. I keep a spreadsheet that is actually mapped out through December of 2014! If something pops up, I know I need to move something else. I am working to pay off my debt so I make big payments to the one bill I’m “snowballing” and I can move money from that slot to the “something came up slot”, without going into the negative anywhere. It works great. I started it (again) last July and have paid off 4 bills and only have 2 more to go on my side. He has other debt, but he handles that himself.

Hello Sarah,

My fiancee is working on paying off his student loans. I am very interested in your spreadsheet that you have, I really think it would work for him (and me when I start to pay off mine). Would you mind giving me some more insight on this?! Feel free to e-mail me. Thank you so much!

Hi Amy, I can’t see your email, but feel free to email me at: hands2work at gmaildotcom…

Please email me the spreadsheet. Please!!! We are a military family getting ready to transfer.

Hi Sarah,

I have been trying to get my spending under control. I am 26 and while I don’t have debt, I have no savings and no RRSPs…I find I am not budgeting and get to the end of the month and poof no money! Your method seems exactly what would work for me (I pay all online as well) and I have been struggling to come up with a long term plan, would you mind sharing your spread sheet template with me also? Jennamr@live.ca!

With gratitude,

Jenna

liked your idea do you think you could email me a copy of your spreadsheet? i’ve been researchingg them but nothing seems to look like it would work. Would really appreciate it thanks

Please find a sample copy of the spreadsheet attached. I have deleted all my own numbers and used round numbers and normal creditors/utilities in their place. I get paid every other Friday. Each paycheck I put in the “paycheck” slot and then whatever amount it is over the norm I put in the “overage”. I add the overage to whatever bill I’m paying off. Now I’m at the point where all my bills have been paid off so all the extra money goes into to savings and then I invest it into a Vanguard Index Fund. In just over a year I paid off all my debt and started investing. I found out that avoiding restaurants and bringing my lunch everyday (plus keeping a loaf of bread and pb&j) in my desk really really helped me pay stuff faster. Restaurants were my weakness. Good Luck!!!

Could u please email me a copy of your spreadsheet to thanks…got 4 kids and need to start saving

I would be very interested in this spreassheet system of yours! This system sounds like it might work real well for me in paying off my debts and student loans… If you are willing, please email me at rachellecate at gmail dot com. Thank you!

Do you think you can email me a copy of your spreadsheet also?

sammx243@gmail.com

I would also love a copy of this spreadsheet! Would you please send it to brittanyl2b at gmaildotcom? thank you very much!

One tool I use to adapt the envelope budgeting system is EEBA. It is a website and smartphone app found at http://www.eebacanhelp.com. It combines the envelope system with todays card-happy society. So far so good!

all fun and games til someone robs your envelopes. My sister swore by this method until she was robbed twice by people she knew. My sister is a educated, manager at a well known retail store.

The same happened to me!

I think it’s time for your sister to get more educated and get new friends.

I am trying this, however I am confused how you go about starting up the envelope system? How do you know how much to put in each envelope ? If you are tight on money anyways how can you just put that much in all at once? I have a family of 3 any suggestions????

First you should figure out HOW you want to divide your money (i.e. your categories). Then regardless of your income, take out a certain amount for each envelope. Don’t be surprised if your bank account balance gets pretty low…it’s okay, because you are training yourself to live off cash. Remember, once it’s gone from a envelope….it’s gone. If you have anything left over, you can roll it over to the next pay period or you can used whatever is left and apply it toward a debt. Good luck!

Start an excel spreadsheet and figure all monthly bills, due date and then divide by paycheck. If you do this on a 3 pay day month then there is a little extra wiggle room. Rather than use envelopes where someone could steal your actual cash, make the automatic deduction in the checkbook for that payperiod then just go back and fill in the date and check number when the bill arrives. As for left over, the checkbook balance shows what is figured in on the excel spreadsheet for groceries, gas and entertainment. When this amount is gone – it’s done until the next payperiod. The remaineder of the check (albiet a small amount) is automatically transferred to savings so it is not accessible. So in short, the balance left in the checkbook is spread out over food, gas and entertainment – when the checkbook balance is zero then no more spending occurs – altough the actual bank account might have some money left in it for the bills that are yet to be paid from that paycheck. Hope this helps.

I am also tight on cash but I have been doing this now for about 2 months and its great. I was over spending on groceries/food and had no idea how much gas I was actually consuming. I budget actual $ amounts per paycheck. If it is a bill that I pay online or is automatically drawn out of my checking I make sure I put that $ in my account, otherwise I cash all of my checks. I have spend for groceries/food, gas/car maintenance, personal grooming, spending for my daughter, savings for my daughter, savings for me. (In addition I NEVER spend any of my change, instead I put it in my daughters piggy bank). I also just started putting the leftover weekly $ for gas and groceries into its own envelope for me to decide what to do later, which I will probably use for savings. Good Luck. I have found this so helpful, I hope you do too.

It might help if you categorize your spending and keep record of it for a month. This way you’ll know which catergories need a bigger share of the money. Pay those off first and then divvy the rest up into your envelopes to save for the future.

I really recommend buy Dave Ramsey’s book. My brother bought it for me and it has step by step instructions on how to determine what goes where. There were categories I forgot about until I ready them and thought “yeah, that’s smart.” This book literally changed my life. If you don’t want to buy it, check it out from the library. I’m about 8 months away from being debt free and I used to have over $20,000 in cc bills.

I’m on online bill payer, but I really want to budget all of my bills, figure out what’s left and withdraw that from the bank to be used for anything non-bill related (ie groceries, gas for the car, etc.) BUT the trouble is getting my husband on board with this….. I’d take away his credit card, but then I can just see an emergency coming up where he’d need it. *sighs* Will keep trying!

My husband doesn’t keep his credit card in his wallet every day. Only on work related trips.

Another thing we do it that i give my husband an allowance every month. He can spend it on what ever he wants no questions asked, no pestering him where it went. When it’s gone it’s gone.

Do you keep his allowance next to his sack in your purse?

Tim, how is that any different than the husband… man of the house, giving his wife an allowance to run the house on and that is it? Whatever works for each household, I say. I still know of husband’s that do just that… give their wife an allowance. Lot of guys I know still stuck in the 1950’s mentality and want 100% control of everything.

Tim,

If the husband would care enough about the family’s economy to join in on keeping track of where money goes I’m sure this type of thing wouldn’t be necessary at all. They’re not saying that they do it to control him or how much he spends, it’s about knowing where your money goes, and when you’re a couple and have joint finances it’s very annoying if one person is going to destroy the other one’s budget work just because they don’t care enough to get on board with it. So an “allowance” is simply a feasible idea to get around this. Works for both parties. Ideally, the husband would make the effort himself to keep track of what he spends so that the couple can keep a functioning, accurate, helpful budget — but if he doesn’t want to then isn’t this a good solution? Or what would you suggest yourself for couples with joint finances where one person isn’t interested in doing budget work? That she (if it’s a woman keeping the budget, because I doubt you’d be upset if it was the man giving his wife an allowance, am I right?) just give up on keeping a budget because her husband is too selfish, lazy and immature to keep his receipts? Yeah, that’s much better.

They could get seperate finances of course, but why do I sense that would only mean so much more work for her? I mean, if the man can’t be bothered to keep track of his spendings, what happens when the kids need winter coats and she’s been saving up her part but he hasn’t saved up his? (Just one possible scenario off the top of my head.) If one partner insists on being irresponsible and ignorant with their money it will effect the other one too, unless they take control of their situation. And yes, it is irresponsible to be an adult human being, and married at that, and not keep a budget. If you don’t realize this and bash on a woman for doing what she can to make her finances work (or work better) then I have but one thing to say to you: Grow up.

I have a system where I keep some extra cash in my wallet, and some in my car (enough for small emergencies). The reason being is if I ever forget my cash card, lose it, or end up somewhere that doesn’t take it. You could implement the same system with him, and then “emergencies” can be taken care of without a card.

I use the same concept, but on a rewards credit card. I have budgeted each category and subtract each purchase each time I make one. Once I get to zero in a category it’s closed. No more purchases may be made. I pay off the card each month so there is never a balance. I realize that spending cash psychologically tends to make a spendthrift hold back more, but by substracting each purchase each time, I achieve a similar effect, and it allows me to get about $300 extra annually in rebates.

I love this idea. This is totally doable. Thanks for such a clever suggestion!

That is what we do. We pay all our bills, groceries, pretty much everything we can with our rewards credit card, but never going over our budget and paying it off every month, so no interest and lots of points. Works great now that we have a friend getting marry in Germany and Colombia we have enough points to fly for free, so no restrains in our budget.

Reblogged this on The Big and Small and commented:

This is awesome. Great money solutions if you have to much month at the end of your paycheck.

We’ve been doing the envelope method for years. I just pay all of our bills online, so I can receive an email confirmation of the payment. I print off a copy and attach to the paper bill and then toss it after the payment has cleared my checking account. The envelopes contain cash for household, groceries, entertainment. We usually purchase a Walmart gift card with the gas money, so we can save 3 cents per gallon. If there happens to be any leftover the following pay period, I just apply it to my household purchases.

Reblogged this on InkPaperPen and commented:

I thought this made a lot of sense. Different from the kinds of things I usually post, but very smart! Especially for me, being a college student and all.

Thanks Inkpaperpen for the reblog!

You’re very welcome! I found the post on Pinterest and had to share it!

My church is doing a bible study on daves program. Its awesome, me and my husband have had trouble a few weeks now cause of christmas but this week has been the first week in 5 years our bank account has not been in the negative! Amazing! It really does work if you put your mind and energy towards it.

I actually do not follow a physical envelope or jar system. I don’t like the idea of carrying cash around. The only cash I have is what I have in a coin jar to which I put in any coins I come across (usually from grocery carts that I come across that people fail to return – coin still in place). My in-laws follow some sort of jar system though.

I had been using MS Money (up until Microsoft gave up on the program). I then switched to Quicken Cash Manager 2011 and been using it since. I don’t use the budget portion of the program as I can’t figure it out to the way that it would work for me. What I do is enter and process through reoccurring transactions (estimates of bills being over what they normally would cost (natural gas $140, electricity 100, fuel 60×2 (I fill up twice a month), internet 35, etc) and even estimated grocery costs per week $125, and investments $400 per week). Whatever I don’t spend eventually ends up in the savings account. I have set this up and processed through in Quicken up to May 31st of next year for now (being when property taxes are due) so I know what to expect on my everyday expenses for the next 5-6 months. Normally in that program you would process payments and charges as you do them but this is how I budget. I adjust the figures as needed.

To clarify: on the ledger of the program it shows what costs have occurred but below today’s date it would show what I am expecting for the next few months (because I processed them instead of waiting for the days to pass by to process them then). If I don’t do this then I don’t have a working electronic budget system that would work for me. It is sort of an electronic envelope system where I did set aside a chunk of money from my paycheque for groceries and everything else for the entire month. I always keep at least $2500 in the chequing account to waive the $12.50 chequing bank fee for the month – but I do keep it above another $500 just to be on the safe side as any dip below $2500 would land me that bank fee. Anything money left over above my set $3000 balance on the chequing account on each of my pay days gets transferred over to the savings account to go towards property taxes or an emergency. This is done after my investments and bills. My investments are used as a last resort backup fund – for emergencies – if my savings account and that $3000 isn’t enough. I hope this all makes sense.

I don’t overspend at all. I am actually a bit of a penny pincher. I do use my credit cards for all purchases but keep a strict set amount to spend. This allows me to collect cash back rewards while I use those cards. I don’t carry a balance every month – paid off in full. Any cash back eventually goes into savings/investments. I also do online surveys when I find time to which the extra cash goes to savings/investments.

I use to be in debt before I got married last year. Back yard wedding without traditional wedding clothes – very simple and not expensive. We were more focused on a downpayment to our first home that we bought on Valentine’s Day this year. Now we only have a mortgage at an excellent interest rate. My goal is to make sure my family doesn’t go through what my parents had gone through and are pretty much forced to face because of their silly money mistakes. My mother is trying to turn things around but my father just doesn’t learn. I want to make sure that we are at least comfortable when it comes to retirement many years from now.

These are awesome ideas, thank you!

My parents took a course offered at our church from Dave and they currently follow this system. They have only been on it a few months. So far I think they enjoy it. They are trying to get me to do it, but all of my bills are paid online. I do have a similar type system for online people.

I have two checkings and a savings (all linked). When I get paid, $100 automatically goes to savings (I never see if hit my checking). As soon as I can, I tally up the amount needed for bills that pay check and put it into my second checking account (my bills account) All of my bills are automatically withdrawn from that account. The main checking I use for groceries, gas, and any entertainment. Then before I get paid the next time around, I transfer what’s left from my main checking and put it into savings. So on Thursday I am flat broke – main checking is zeroed out – and 12am on Friday starts a new budget cycle.

I’m pretty used to this system, but I always over-spend on entertainment – Dave’s system might not be so bad for this area. I do find it harder to spend cash than swipe plastic. Alright, I’m in the mood to budget now. Thanks for getting my juices flowing!!

This is a great idea.

I opened a separate account for Bills. Each paycheck I transfer all the money I need for bills. Kinda like and Electronic Envelop. I like to know that all my bills will be there no matter what. It’s nice because I don’t have to sift through other expenses to find my bills.

Rather than using cash, I set up a separate bank account. I get paid every Friday & deposit my paycheck to my local account. Every Monday, one-fourth the amount of my total monthly bills gets automatically transferred to a second account. All my monthly bills get paid out of the second account, and I can use what is left in the local account for gas, groceries, and other extras. When there is a month with 5 paydays, I transfer the extra week’s auto deposit into my savings account. It has been a huge financial life-saver for my family.

I’m a college student so my income is really varied. I have to pay rent, cable, electricity, credit card bills, gas, and food. It’s hard for me to pay it all, and I have to get help from my mom every month. I don’t like doing this because I want to be independent. Do you have any suggestions of how I should do this system?

I totally agree that using cash is best to keep your spending on budget. Another great thing to do is automatic payments into a government retirement plan. Every pay day a set dollar amount comes straight out of my bank account and into a registered retirement plan. You get pretty used to living without that money since it comes out as soon as you get paid. Then you deal with what is left over and divide it where it needs to go.

Reblogged this on 4THELOVEOFDESIGN.

I’ve done this for years, Just this year I set this up in account and all my bills on the budget plan, they withdraw what they need for each month and I have what is needed deposited each month.

I do this! And it works! However I started with 5 envelopes and am up to 9 but some are seasonal and I put in less off season. Its fun to physically save the money 🙂

I really like this idea! However, I would not put actual cash in an envelope. I have had too many occasions of misplacing cash, so I personally don’t think it is a good idea to have more than $20 or $30 in your wallet, unless you need it for a specific thing. If you lose cash, it’s gone. In the bank, it’s safe!

I use a virtual envelope/budgeting system along with a check register on my iphone. It syncs to my husbands ipad at work and his android phone so we are always on the same page! In the past 6 months we have cut our debt by 50% when before we were having to forward money to make it until the next paycheck. It has made a huge difference in our lives and now we are looking forward to buying a house! If you had asked me 6 months ago if we could do that i would have laughed.

I will never go back to blindly spending our money or not using the envelope system!

I’d love to know more about your virtual budgeting system. Email me at mtolman2 AT yahoo

This sounds interesting. Please share more on the app!

I must say I love this and have been working on this system for a while now. This entire concept is really brought to much more light by reading David Ramsey’s book! I’ve read it twice and listen to the CD’s in the car 3 or 4 times, to make myself rehear and keep motivated!

Reblogged this on Love is all you need… and commented:

Maybe going to try this once my new job starts. It seems great plus would be a great way to start saving up for things. It’s so easy to simply sign in online and transfer money from savings to checking. Maybe this will work better!!

I am a full-time student and my husband works full time. We have two kids. We started this system about a year ago and now we are buying our first house! I can tell you it really works if you stick with it! You won’t believe the extra money you find!

Awesome idea!! I went from single (i.e. no budget) to coupled and managing finances. I was looking for a way to keep the spending reined in so we could save money and this is a GREAT idea. I’m sure it’ll need some tweaking as we go along but it’s a fantastic start. Thank you for the post and your added notes!

I created a spreadsheet with each bill and it’s due date. Since I’m paid every two weeks I’ve broken down how much each bill I will pay each paycheck, either by automatic draft or bill pay. If that’s weeks bills comes to $800 and I’m being paid $1150 I will pull out $200 to use for groceries, gas and misc. items and won’t use my debit card at all. Out of cash is out of cash. I like the envelople system so I can see exactly what I have to work with within each catergory.

We did the Financial Peace University class by Dave Ramsey and it was awesome! I’m a stay at home mom so i budget my husbands checks. He works two jobs and it works out to where he gets a paycheck every week. I budget the entire month ahead of time and break the month down into weekly budgets so that each paycheck is planned out before my husband even gets paid. This way if something comes up i know whether or not we can afford it. Also, I try to allot some savings and paying down a debt in each check’s budget even if it’s only an extra $25. It’s still goes towards our ultimate goal of having a savings cushion and being debt free. We use the envelope system for variables like gas, groceries, and entertainment. I budget everything down to the last dime and we live paycheck to paycheck. I’ve found we’ve paid down almost $3,000 in credit card debt and have a little emergency cushion of $500 in case we blow a tire or something unexpected comes up. We still have a ways to go but this system has really helped us get a hold of our money. It’s like Dave says “If you will live like no one else, later you can live like no one else” and I intend to!

For those of you who find the cash system doesn’t equate with today’s credit/debit card culture, there’s actually a virtual envelope program you can use. It’s done by a Christian Organization called Crown Financial (which is affiliated with Focus on the Family). It’s called Crown Mvelopes. You can connect it to your bank accounts, credit card accounts, etc. It can’t make charges but it can see your purchases. The great thing about it is that it keeps up with your budget, and creates envelopes for every category. Then you simply drag your purchases into their correct envelope and it updates the amount left. If you go over, the amount is in red, and you can transfer money from a different envelope if needed. It’s soooo helpful for those of us who don’t want to give up our debit cards! And btw, it’s basic use (which is what I use) is free. You can pay for more features but everything I descibed is completely FREE. 🙂

Look it up: http://www.mvelopes.com

i did this method in my early 20s and it really paid off.

This system has worked great for me. I’ve used it for the last 25years starting at the young age of 10(babysitting money, birthday, Christmas etc…)

Nice Tips for saving!

The envelope system is wonderful. I use it for my monthly budget. I also use it when I take a vacation (having envelopes for hotel, food, souvenirs, etc.). I always end up with money leftover rather than running short of money, which is what always happened before. Most important, I can account for everything I spent rather than wondering what happened to it all. For my monthly budget I have a spreadsheet which lists across the top all of my expense categories (mortgage, electric, cable, water, sewer, trash, groceries, etc.). I have these items grouped according to how they are paid. My mortgage comes directly out of my bank account. My utility bills are paid online. So I leave enough money in my checking account to cover those expenses. The rest of my paycheck is taken out in cash and sorted into the various envelopes for gas, groceries, clothing, personal allowance, etc. This works great for me. The money is there when a bill is due, and I usually have extra money at the end of each paycheck……mostly because of one of basic truths listed up above: it hurts more to spend the cash than to swipe the card. I find myself not wanting to part with the cash. 🙂

I am definitely a believer of this concept. My sister tought me this maaaaaaany years ago a she uses this process to buy a home (cash) and raise her credit score by paying off bills. Our family has done it time to time. But then the convince of swipping a card takes over! This post as motivated me to try again since we are saving to move!

I took his class and it was amazing. He has 7 steps to follow make sure you start an emergency fund. In 9 months we have paid off 3000.00 in debt and caught our monthly bills and started an emergency fund. TAKE HIS CLASS TRUST ME YOU WON’T BE SORRY. Check with your church. Most important envelope is giving you get what you give

I have to say I use Dave Ramsey and my Fiancé and I have paid off nearly $50,000.00 in debt. We live by this system and have had to learn to be very disciplined, which takes some time, but to see that our bills are being paid off and living with in our means is amazing.. we are in control of our money, not our money in control of us!!! Good luck to all and be patient!!

I grew up watching my grandparents and parents using the envelope system. It was a success for my grandparents, but not at all for my parents. I have my own system for budgeting. Right now it’s simple…..hope to make enough to cover the bills for the month. No clothes or entertainment. What I can’t believe is that so many people think that going to the bank is a hassle! It’s not a big deal…..especially if you’re trying to budget your money.

i guess this would be easy if you get paid multiple times a month.

same principle applies if you are paid monthly. being paid monthly means you REALLY have to plan. it makes MORE SENSE to use this method being paid once a month.

I do a notebook system, we get paid by direct deposit also…I never take it out of the bank but I look at the amount of the money on said paycheck.. on each bill or extra (say cello lesson) or amount for gas or grocery to be used for that pay period and make a notation by that category and deduct that money from the amount in the bank. Placing the balance in bold, so we always know exactly what is going OUT and what amount is left to use after everything has been sorted out!!! There is NO cheating or using extra. PLUS MONEY SAVED FROM NOT HAVING TO MAKE TRIPS TO THE BANK……Good notebook and list all bills per page for the entire month ..bottom place bank balance AFTER ALL BILLS PAID and date

I am 19 and have been doing this for a year now. If you just give it a chance it will change your whole life! I am so pleased with my system I couldn’t go back to my old ways even if I tried. I grew up with my family over spending not paying bills and fieling bankruptcy not once not twic but three different times. I decided that I didn’t want to go down the same path! Take Control!!

Reblogged this on carlsonsblog.

The funny thing about this whole envelope idea is…. I was telling my hubby about how I use to do this when I was a single mom of two & was on a very tight budget!!! He thought I was nuts!!!! It always worked very well! Can’t wait to share this with him:)

There is a website which we use called Budgetfocus.com which is the exact same concept except done electronically. Really works!! There is a yearly fee but money well spent. Very easy to set up envelopes and automatically divides money into envelopes as necessary. Highly recommend giving it a try.

If committing to do go all or nothing on this plan scares you or you just think you can’t do it try this. Just pick two areas to envelope. Gas and groceries are a good start. I actually buy a Walmart gift card for gas each paycheck. Our Walmart gas pumps still give a discount if you use a gift card. Stays in an envelope marked gas. The grocery one has saved me hundreds of dollars. Go to the grocery store with just cash. No cards, no checks. You will NOT overspend. Once you get command of the two envelopes then sneak another one in. Worked for me. My next budget drain was breakfast/lunch out while at work. So that was my next envelope. After that I added family meals out (which we cut down a lot because we were enjoying cooking at home because I was meal planning and we always had what we needed to cook a great meal). Anyway, this is working for my family. Baby steps for us but it was almost like a game to see how well we could do! Good luck to all!

\

When you go to the store with just cash on hand are you having to calculate your items as you go so that you know you have enough? I would be SO scared that when I go to check out I had more items then money

Tracy I’ve been doing this for a while on my own and now i’m teaching my mom how to do it too…because she constantly and mindlessly fills her cart without any budget or list and then is SHOCKED when she has to swipe $200 at the check out counter. I make a list and prioritize the list so that the most important things are on the list first. Then we head to the grocery store with the calculator in hand. As we add items to the cart I calculate the ongoing total. If we have $100 in cash to spend I start announcing the total at $50 so that she knows we need to start deciding between needs and wants. It’s really helped and we’ve noticed that we have more groceries and we spend less. It’s just more efficient for us. Hope it helps. Also when you start paying more attention to how much things actually cost you tend to be more frugal and more aware of things you WILL not compromise on no matter the price…like toilet paper or other items that require you to purchase the “good stuff” lol

I have always paid my bills this way. Mr Ramsey nor anyone else taught me this, geez, wish someone would call me a genius :)! We live on a very small amount of money and my husband only gets paid twice a month. So, I budget out my bills and stash away the cash allotment each pay period . At beginning of the month, I redeposit the money and pay my bills (all of my bills are due the first week of the month). We are unable to allot money for monthly clothes or leisure activity so we choose one activity every few months and save for it over a couple months pay checks.

I agree with the envelope system promoted by Dave Ramsey. The part that I can’t figure out or find answers to is withdrawing specific amounts of cash. My husband and I’s income comes in the form of a direct deposit. Do I then go to the bank with a note that says how many of each bill I need to withdraw (ex. $50 in one dollar bills, $40 in tens etc)? Moreover, what about categories that don’t divide out into a product of 10 for each month? I tried doing a cash system before, but felt like the bi-monthly bank trip with detailed request was a bit of a hassle and well..rather bank robber-esk. haha. A second issue I’ve run into is how to work this system between my husband and I. Do we keep and take separate envelope systems for when each of us go to the store to pick up something without the other? I’m not sure if I could get my husband to put down the ease of the debit card! haha. This post and comment section seems to have lots of knowledgeable and experienced envelope budgeters on here. I’d really appreciate anyone that could answer these issues! I would like to implement this system (and savings) into our lives if we could. Thanks! 🙂

My husband’s check is direct deposited as well, and yes, I go to the bank twice a month and withdraw the money that I need. (Tell the teller about your system, she will be so interested in how you do it, that she won’t think twice about you asking for certain denominations of money!) And yes, definitely, separate yours and your husbands spending expenses. Hope that helps answer some of your questions!

We’ve been using this system for years and I love it! Aside from automatic allotments from each check (for vacay, Christmas, emergencies & savings). We use the envelope system for car maintenance, tags, home improvements, piano lessons and kids clothing fund. I love the kids clothing fund the best. I put x amount of money into each kids envelope twice a month. They can use it or “roll it over.” When they decide to use it and they don’t have enough for what they want, they must use their part-time job money to cover the overage. No more fighting about clothing. They are old enough to know what clothing I deem appropriate. If it isn’t, it goes back. No more tears!~~

We have been doing the envelope system for years. This is apart from our automatic allotments out of our checks ( Christmas, vacation, savings and emergency). Our envelopes are for car tags, kids clothes, oil changes. piano lessons, home improvements. I think my favorite of these is the kids clothing envelopes. I put x amount of money in each envelope twice a month. The kids can either use it that month or “roll it over” to the next month. If they use it and they need more, it comes out of their part time job money. This has saved many of headaches when it comes to shopping with them.

How do you figure for bills that are yearly and not monthly(like auto tags, road service renewals, etc, also car insurance that is every 6 months – having two cars it’s like every two or three months)?

Add all of those bills that are once a year and divide by 12. Put that much away every month. This way when the bill is due you have already saved the money. if you truly budget all of your other money you can just leave it in your account. There is no danger of spending it because you already know how much you will spend on other categories and won’t touch this money. Hope that helps.

We have an envelope for those bills (like air & heating services, cars, broken garage doors) also and add to them with each paycheck. For example, we have envelopes labeled “house” and one with “Cars” and the money inside is used for tags, tires, repairs, etc. You can divide by 12 like Cindy mentioned, or put more in to cover unexpected repairs (like a blow-out and you need a new tire) because according to Dave’s book, those things don’t technically quailfy as an ’emergency fund’ situation.

My aunt has been doing this for years and it works so well! Once she told me about it, I started doing it and it really did help me figure out my finances! Best part is – I wasn’t overspending! I definitely need to do that again!

My company allows you to direct deposit in up to three different accounts – I have a college fund for my son, a savings account and a regular bill paying checking account. I never even miss the money, because I never see it – my monthly budget only comes out of the checking account.

What Dave Ramsey book would you suggest reading? I am in my early twenties and horrible at saving but I’m trying to turn over a new leaf!

Dave Ramsey – Financial Peace. We took the course and it was totally worth it! If you can be strict with yourself, you could try the book first. If it is hard to be accountable, then check out the class.

Dave Ramsey- Total Money Makeover!

I used the envelope system years ago and that was the best way I found to budget my family and keep track of my cash. In my grocery/household envelope I would put in a weekly amount and any money left over stayed in the envelope. This was how I would pay for garbage bags, detergent and other household items. At the end of the month I would take any extra and put it in the “extra cash” envelope. Right now we are super tight on money and I am going to start to use the envelopes again with my pay this coming Friday. I really like the notebook and may use that instead of the envelopes, except for groceries. Thanks for explaining this so well and for putting a modern spin to it.

I do the same thing basically, except I use a coupon sorted with the tabs. Fits easily into my purse

I have done the envelope system for over 8 years now and LOVE IT.

It keeps me out of trouble. Each pay period (every 2 weeks) I place the

money I need for that bill in the envelope for that bill only and than I know

what is left in my checking to spend for the rest of the month. I have got myself out of

$65,000 in credit card debt by doing this and it took me 6 years and I am still

using the envelope system.

My sistet has been doing this for years and has worked wonderfully for her.

So, if I pay all my bills online, how do I use the envelope system?

All of our bills except two are all paid online as well because many people “waive” fees if you pay online. That’s why we like YNAB, so whenever you pay a bill, you log it and it comes out of the category.

So we assign $50/month for electricity.

This month it was $38, so we paid it, the extra $12 carries over to the following months’ electric category, and in the winter when heat is on and the bill becomes higher, we have the $12 each month extra in that category for if it goes over $50.

Cash just didn’t work for us, mainly because of the lack of convienece of getting it from the bank, and everything being paid online. I would highly recommend looking into this. it’s been AWESOME for us.

http://www.youneedabudget.com/method/rule-one

You leave the $$ in your bank account that you pay online and just get out the cash that you would write checks or use a debit/credit card for. We have done it this way for over 3 years. You create a written budget that dictates where everything goes then can decide which go directly out of the account and which you use cash for.

Husband and I don’t do well with physical cash. We started using YNAB (http://www.youneedabudget.com) and it’s be fabulous. if you’re tech savvy and want to do the envelope system without carrying cash, check it out! it’s been awesome!

Whatever you don’t spend one month, do you carry the money over to the next month so you have a little extra? Or do you put that in savings and then just have the same each month?

Hey Brooke, I roll it over to next month!

This is wonderful…my parents used this system all the time and let me watch as they counted the money and entered it into each envelope. I am going to give it a try as I also seem to be asking myself where the money went?!?! Thank you!

Cash is a wonderful prohibitor, but if you are using a debit card and/or online bill pay, check out this resource: http://www.mvelopes.com/crown/home This offers a free virtual envelope system. We’ve used it for years and now our daughters are old enough to make use of it.

I Have to try this, not matter what. So at list i can see some money build 😦 cause we are bad in the area, we can harly see money to save, everything came weekly, and everything go 😦 so i have to try this …thanks !!!

I love the accountability of a cash allowance… I’m just curious how do you handle shops that include multiple areas of spending like Target or WalMart? I buy groceries, household items, clothes and gifts at stores like this. Thanks for any advice!

I’ve noticed that a lot of stores are now itemizing their receipts ( I think because of taxes etc.. in MI food isn’t taxed but clothing is). When I do my shopping, I estimate what I’ll need, make sure I’ll have enough in whatever envelopes I’m using then when I get home I go through and redistribute what I have left over back into their appropriate envelopes.

First, for us, our food and household supplies are categorized together, since I have always bought them together. When I shop at Target, Walmart, etc., if it is a bunch of stuff from different categories (food, clothes, gifts, etc.) I separate my categories at checkout, so I have 2 or 3 different orders. This helps keep me in my category specific budgets.

My dad used to do this with real envelopes! When bills came he deposited the money in the bank, noted what he took out on the envelopes, and started over. He always knew what he had and where it was going. I like this updated version. When I start a new job, I’ll set this up!

I do this and it works soo well!

Btw, I just showed my mother in law this post and she love this idea! She says thank you – LOL

http://coordinatedkate.wordpress.com

That’s so great!

My husband recently came home telling me he wanted to do an envelope idea and have me hide them from him because he tends to overspend. I knew it would be a good idea but still wasn’t sure how to do it. Thank you for posting this.

How many trips would you say you make to the bank each month to get the cash? My husband and I each get paid twice per month, so that’s four pays per month, each by direct deposit. I can see myself getting frustrated having to go to the ATM/bank teller once a week to get cash. I like this system and I know it would really help us, but I just wonder if it ever feels like a hassle.

I would suggest withdrawing enough for a two week span so that you go every pay period.

I just found this post via pinterest. I am a SAHM, so my husband’s pay is the only one that we have coming in. I will suggest that you figure out what you’re going to pay with each check. With the first paycheck of the month, we pay his car payment, the car insurance and phone bill. Then we fill our envelopes. The second check is my car payment, internet and envelopes. I would think maybe in your situation, figure out if maybe one check could be bills and one could be envelopes. So, say use your check to fill the envelopes and go every two weeks to the bank. I am going back to work soon and I think this is going to be the approach we take. One of our checks is for bills and the other for envelopes.

Sometimes, yes it’s a hassle….but being debt free….not really a hassle!

My husband and I both have our pay direct deposited…mine once a month, and my husband’s once a week. We have taken this concept and switched it up a bit. We use a notebook, and have every bill that is due each week written out for the entire month. I know how much our income will be for that month, and how much our total bills will be also. Then, I know how much will be left over every month for any extras such as shopping and entertainment. Sometimes I will even get a month or so ahead set-up. For example: For the first week of the month, I would have something like, 1st…House Payment $$$$.$$, 3rd…Car Payment $$$.$$ and so on…each page is a different week. This way, I can look ahead and see what is coming due in the coming weeks! Then, if something comes up, I know if we can afford it or not! Make sense? I hope I didn’t ramble too bad! Works for us!

My husband and I are on a natural budget… meaning, every two weeks he gets a paycheck and we budget that thing to the last DOLLAR because we have no other choice. 😉 Every month is that tight! All our bills are paid online, and we share the same checking account. We want to save money, but we’re lucky if we come down to having $50 in the account by the end of two weeks. So we do “envelope budgeting, inside out,” meaning, we take out $20 when we can and put it in an envelope to save. The money in our account has to get sucked up and dried out, but hey, envelope money builds up… it works. 🙂

we are also on a very tight budget, one thing we do for savings is we save all of our one dollar bills, that adds up also over a period of time. We dont have extra money to go out to eat or have a date night very often, we also have a jar that we keep all of our spare change in and when we have saved a hundred dollars in change we take it to the bank and cash in and have a date night

I just posted a financial spreadsheet on my blog yesterday that I think may be able to help you. Check it out and let me know if you’d like for me to send it to you!

http://coordinatedkate.wordpress.com

How do you budget if you have no idea how much money you’ll make in a given month? I’m a substitute teacher and I either get days or I don’t. Anyone have a similar experience?

You could do it based on a percentage system versus a certain amount each check.

Dave Ramsey has a section in his book “Financial Peace” for your situation as well. Make a budget for all the same categories as anyone, them list them in order of priority. When you get paid start filling envelopes and paying bills in order of priority. When the money is gone you may not get to categories like beauty or entertainment this month. Hope this helps.

Great book for anyone to check out.

Oops, Allyson, I just posted what we do on Ashley’s post right above. Sorry!

I’m not sure if this will help. But my paycheck was always a certain amount. So we would budget for that amount. Then anything over that would either go towards debt, a bill that didn’t get paid in the budget, or to something we couldn’t afford to budget for. That way we still budgeted what we could and had a little extra to splurge or pay debt at the end.

We have been living on the envelope system for over 3 years now and it has saved our family a fortune! We paid off all debt (besides our mortgage which we refinanced to a 15 yr) and have paid CASH for 2 vehicles with what we can save on Dave’s plan. I do in home day care where my kids only pay if they come, so my income is never the same either. It took a few very pinched months, but what we finally decided to do was to use the money I made in the current month and budget it for the NEXT month. Then, we knew exactly how much we could spend. The first couple months of making this transition were tough because we had to pretty much go on NO income for me for a little over a month, but once we did it, it was well worth it – and now it is just part of the plan. I will never go back to a non-cash envelope system again and it is how I will teach my children to live as well. Hope this suggestion helps.

If only Dave Ramsey could run government spending as well….. 😉

I am also a substitute teacher, and we get paid monthly in my state. First, as soon as I am able, I calculate what my next check will be after withholdings. In my situation, that gives me a few weeks to draw up my budget, but your pay periods may not be behind like ours are. Immediately upon getting my check, I pay all of my bills, regardless of whether or not they are due soon. Then, I budget for gas, groceries, and savings, in that order, depending upon what is left over. I move cash to envelopes for gas and groceries, and electronically transfer money to savings from checking. If there is anything left in my checking account at that point, I consider it “fun” money, which generally goes toward movies and eating out. Since that’s all that’s left in there, I have no danger of overspending in that category, so I use my debit card. When I still carried a balance on my credit cards, I prioritized paying them off above all else, but I have MUCH more wiggle room now that I don’t carry that debt.

In other words, after bills and gas (which are pretty well fixed expenses for me), everything else varies month-to-month.

Most companies perfer you pay your bill with a check or money order rather than sending cash and it’s better to pay by check rather than cash so that it can be tracked. Lets use the picture as an example: you put $50 in the sleeve for the phone bill… when it comes time to pay for the phone bill, do you put the cash back in your account in order to write the check?

Ashley, you make perfect sense/cents. I actually pay my bills using online Bill Pay right off the top. That way, I receive a confirmation email once the payment is received and then another one once it is processed (for tracking purposes). A percentage for my savings is also separated right off the top. I then use my envelopes for everything else. Right now my categories are the following: restaurants/entertainment, travel, groceries, personal maintenance (hair and/or nails), clothes or home improvement projects. Hope this helps!

In our case, we have a few things that are generally paid on the debit card through the paycheck but can be paid for with cash easily-like gas and groceries. We pay our trash bill every 6 months on the debit card, but I set the cash aside monthly. When it comes due I just pay the bill and move the cash to the grocery budget. It sounds confusing, but as long as I don’t get behind it works really well.

Ashley, I adjusted our budget sheets to 5 days AFTER each paycheck, which means for 5 days it sits in the bank while I finish the budget from that paycheck and gives me time to get to the bank for the cash before that paycheck “starts”. Our budget plans go from the 5-20, and 21-4 (my husband gets paid on the 15 & 30). I have 2 seperate sheets with the bills needing paid between those dates printed out and in a sheet protectors. I use a dry-erase marker to fill in the blanks (variable amounts for each month; like electricity, gas, water, etc) and budget it out to a zero based budget. For us, that means the leftover of one paycheck goes to savings, the leftover of the next one goes to an extra payment somewhere and we live paycheck to paycheck. I definitely suggest reading Dave Ramsey’s book because there are several examples of budget sheets for fixed and varried monthly incomes. Let me know if you have any questions!

Sorry, posted this on the wrong person’s question.

Ashley, for your situation we still use our sheets to budget and leave any money in the bank for bills we pay by check. Say our electricity bill is $73.28 – it still gets budgeted out, but I don’t withdraw that cash. It stays in the bank. I make a list of categories that get cash and tally up what and how many bills ($50, 100, 10…) I’ll need for those 2 weeks and just get the cash for those categories. Hope that helps!

use money orders, the money is not there to temp you, you can keep track of it and businesses are happy to accept them…. i would recommend getting them at the post office, they only charge around .60 cent per and the bank charges around 3.00

You can also get money orders from a credit union. Most credit unions only charge a $1.00 no matter the amount.

Depending on what time of checking account you have, you might be able to get money orders for free. I know my checking account through Wells Fargo allows me to do them at no charge.o

I used to do this all the time and it works really well. Until I started using my debit card for everything. Now I use spreadsheets and planners to itemize purchases and prevent splurges – hahaha!

http://coordinatedkate.wordpress.com

Just checked your blog out and girl, we could totally be friends. My planner is color coded like yours. Please feel free to stop by anytime and I look forward to reading more of your posts.

Thanks for posting, it reminded me that I needed to post my latest update up about the progress of the Envelope System:) I love that you are doing something similar. Just recently, I started a vacation account too, which I’m really excited about. Since you already do something similar, do you have any tips you would like to share? I’m sure the people who visit She Makes Cents, would LOVE to hear how it’s working for someone other than myself. I think I need to refine my categories a bit. As mentioned in the post, this was shared from the brilliant Dave Ramsey. I stumbled upon the picture from Pinterest. It comes from a cool blog called Tales of the Coop Keeper…you should check it out! The picture linked to the sites, but to make it more user friendly, I kept the original links and added some at the bottom of the page. Thanks for stopping by and please come back again!!

The She of She Makes Cents

Oh I love this idea! I am going to try it on my next paycheck! Thanks

I started last check and it has forced me to really look at where my money is going. I now ask myself, “do I really need that”? I’d love to hear how it works for you. Please keep us posted and good luck!!!

We have a similar system. We found a whole bunch of different shape jars and we put our moneys in them. On each jar has a picture or a cut out of a word that describes what the jar is for. We use this for the things we pay cash for like gas, food, the sitter and so on. We also have jars for the things we are saving for. A new bed and bedroom set for us, a playset for outside, and new living room furniture. It’s really helped us visualize the things we do. With our sitter we have to pay her weekly on Mondays. I don’t get paid weekly but we take $130 and fold it in half, put a post it not on it and paper clip it “shut”. we then drop each bundle into the jar. When Monday comes around, I grab a bundle, double check it..and hit the door. We do this twice a paycheck for each of our paychecks. We know we will always have money for our sitter no matter what happens. 🙂

I love this concept. I am definitely going to try this.