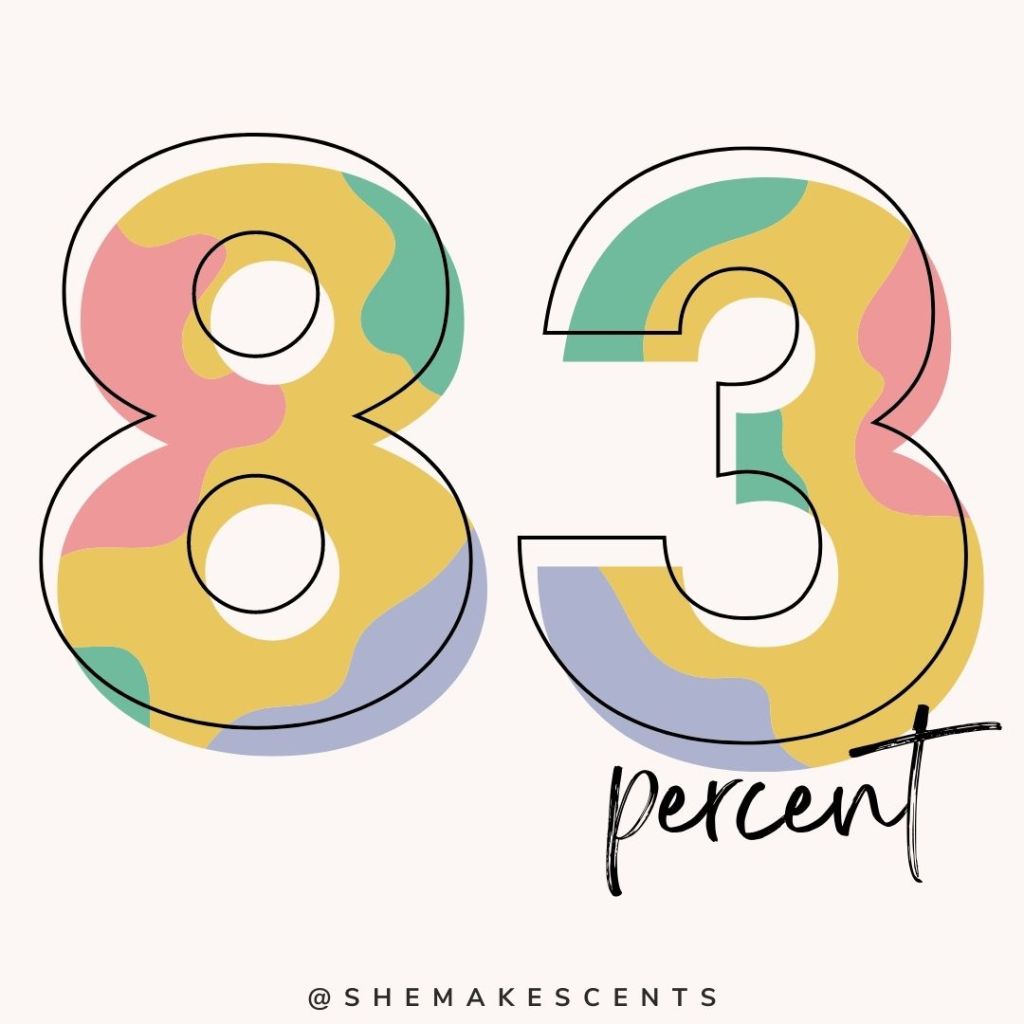

In 2020, 45% of my mortgage payment applied to interest, and the remaining 55% was applied to principal. However, in 2021, I turned that number around SIGNIFICANTLY to reflect 83% of my mortgage payment going toward the principal and only 18% going to interest.

2020: 45% interest/ 55% principal

2021: 17% interest/ 83% principal

…talk about making your money work for you!!!!

How do you ask?

I started making a few easy changes and you can too…

☆ Round Your Payments Up: Rounding up to the next highest $10 or $100 amount can significantly help reduce the term of your mortgage by putting those small amounts towards the principal.

☆ Make Biweekly Mortgage Payments: There are 52 weeks in a year and 26 biweekly periods. That is the same as making 13 regular monthly payments. As it turns out, that one extra payment per year can add up – a lot. Biweekly mortgage payments will allow you to make one full mortgage payment directly towards the principal. You will be reducing the amount of interest you will have to pay over the life of the loan.

☆ Set a goal for your mortgage: I knew at this time last year that I wanted the balance on my mortgage to be a certain amount by the end of the year. To accomplish this goal, anytime time I received “extra” money (i.e. tax returns or unexpected income) I always made sure a great portion went toward my yearly money goal. That is in addition to all of the money I saved doing the #SMCmoneychallenge, of course.

☆ Get to Know Your Amortization Schedule: I have never pulled up my mortgage amortization schedule more than I did this year. It was important to me to know the exact number/percent of my mortgage payment was being applied to my payment AND then make sure that any extra money I applied to the principal was always MORE than what was being applied to the interest.

Many people get caught up in waiting until they have saved a large lump sum before many any type of move towards their goals. I am proof that if you apply what you can afford, be it an extra $5, $500, or $5000 because even a small step is still a step in the right direction when it comes to goals.